Listen to our 6-minute conversation about this articles content in our Deep Dive if you are short of time

The Two-Faced Bean: The Ubiquitous Legume

It begins as a humble seed, nestled in the dark earth. Yet from this simple legume—Glycine max—springs a global empire of immense, almost invisible, power. The soybean is the ghost in the modern machine. It is the protein in the chicken nugget and the farmed salmon, the emulsifier in the chocolate bar, the oil in the mayonnaise, and the meal that fattens the pig for the ham-and-cheese sandwich.¹ It is the feedstock for the biodiesel that fuels the city bus, the adhesive in the formaldehyde-free plywood that builds the home, the protectant that extends the life of concrete highways, and the base for the ink that prints the daily news.²,³ It is everywhere and, for most, nowhere to be seen. This ubiquity is the soybean’s triumph and its tragedy.

At its core, the story of soy is a story of a profound paradox. It is a biological marvel, a nitrogen-fixing legume that enriches the soil it grows in, reducing the need for synthetic fertilizers.⁴,⁵ It is a nutritional powerhouse, a dense package of high-quality protein and oil that has become a cornerstone of the global food system.⁶ Yet this “miracle crop” is also a primary agent of ecological destruction and social disruption. It is the engine of the global protein transition, enabling the mass production of affordable meat, but in doing so, it has carved a path of destruction through some of the planet’s most vital and biodiverse ecosystems, from the Amazon rainforest to the Cerrado savanna.⁷ It is the foundation of a multi-billion-dollar industry that feeds millions, yet its chemical-intensive cultivation poisons waterways and has been linked to devastating health crises in the communities that border its vast monocultures.¹

This investigation argues that the modern soy industry represents a colossal system of externalized costs. The immense profits reaped by a handful of powerful corporations are built upon the degradation of global environmental commons, the erosion of public health, and the displacement of traditional communities. The very structure of the industry—its hidden, ubiquitous nature—functions as a key mechanism of its power and a structural barrier to accountability. Because consumers rarely see or recognize soy in the final product, their consumption choices are decoupled from the profound environmental and social impacts of its production. This knowledge gap creates an accountability gap. If consumers do not know they are consuming a product linked to deforestation, they cannot exert the market pressure required for change. The industry’s deep integration into non-food industrial supply chains further insulates it from consumer-facing activism, making reform exceptionally difficult.

To understand this two-faced bean is to understand the intricate, and often brutal, trade-offs of our globalized world. This report will trace the soybean’s journey from an engineered seed to a global commodity, examine its planetary impact, map the architecture of power and profit that governs its trade, and critically assess the fraught search for a more sustainable future.

Part I: The Industrial Engine: From Engineered Seed to Global Feedstock

The soybean’s global dominance is not an accident of nature but the result of a century of agricultural and industrial optimization. Its journey from a carefully engineered seed to the primary fuel for the world’s livestock reveals a system designed for maximum efficiency in converting land, water, and sunlight into the two core components of the modern food economy: protein and oil. This entire chain reveals a system designed for industrial scalability, where the biological and ecological complexities of agriculture are subordinated to the logic of mass production. The soybean itself has become less a crop than an efficient biological chassis for delivering standardized, fungible units of protein and oil to other, even larger, industries.

A Plant’s Progress: The Agricultural Lifecycle

The story of a modern soybean begins not in the soil, but in the laboratory. The vast majority of soybeans planted today are products of biotechnology, specifically engineered for herbicide tolerance. Globally, 74% of all soybeans grown were biotech varieties in 2019, a figure that has climbed to a staggering 96% in the United States, the world’s second-largest producer, as of 2024.⁸,⁹ This technological lock-in is the first critical step in the industrial process, wedding the crop to a specific chemical regimen, most notably glyphosate-based herbicides, which can be sprayed liberally on fields to kill weeds without harming the resistant soy plant.¹

Once in the ground, the seed needs only warmth and water to germinate, with soil temperatures needing to reach at least 12°C (54°F).¹ Within days, the plant exhibits epigeal emergence, pushing its first two embryonic leaves, the cotyledons, above the soil surface (VE stage).¹⁰,¹¹ These initial leaves provide the energy for the seedling to establish itself for the first seven to ten days.¹² From there, the plant enters its vegetative stage (V stages), rapidly putting out trifoliate leaves (leaves with three leaflets) and growing taller. Farmers aim for the plants to grow quickly and form a dense “canopy” that shades the ground between rows, a natural method of weed suppression.¹

About six to eight weeks after emergence, the plant shifts to its reproductive stage (R stages), producing small, self-pollinating flowers.¹³,¹⁴ This is a critical period when the plant’s nutrient needs increase dramatically to support the development of pods and seeds.¹ While soybeans, as legumes, can “fix” up to 60-70% of their own nitrogen from the atmosphere through a symbiotic relationship with soil bacteria (Bradyrhizobium japonicum), farmers often apply fertilizers containing phosphorus (P) and potassium (K) to maximize yield.⁵,⁶ The cycle culminates in the fall, as the days shorten and the plant senesces. Its leaves turn yellow and then brown, eventually falling off to leave the mature, dried pods exposed and ready for harvest.¹ At this point, enormous machines called combines move through the fields, cutting the stalks, threshing the beans from their pods, and collecting the harvest, which is then transported to grain elevators and processing facilities.¹

The Great Crush: Anatomy of an Industry

The harvested soybean holds its true value locked inside. To release it, the vast majority of the global crop undergoes an industrial process known as “crushing.” This is where the bean is mechanically and chemically deconstructed into its two principal, and highly profitable, components: high-protein meal and vegetable oil.¹

The process begins with preparation. The raw beans are thoroughly cleaned to remove stones, dirt, and other field debris.¹⁵ They are then cracked into smaller pieces and dehulled, a process that removes the outer fibrous shell.¹⁶ The cracked meat of the bean is then conditioned with heat and passed through massive rollers that flatten the pieces into thin flakes. This step is crucial, as it maximizes the surface area and ruptures the cell walls where the oil is stored, making it accessible for extraction.¹⁵

The heart of the operation is solvent extraction. The flakes are moved to a large extractor where they are washed in a countercurrent of commercial hexane, a highly efficient and recoverable solvent.¹⁵,¹⁷ Hexane is a known neurotoxin, and although it is classified as a “processing aid” and thus not required to be declared on food labels, its traces can be found in final products, a fact largely unknown to consumers.¹⁸ The hexane dissolves the oil from the flakes, creating a mixture called “miscella,” which is typically about 25% oil and 75% solvent.¹ The now oil-free flakes, still saturated with hexane, are sent to one processing line, while the miscella is sent to another. The two streams are then separated. The miscella flows into a distillation system, where, under a high vacuum to lower the boiling point, the hexane is evaporated from the oil, condensed back into a liquid, and recycled for reuse.¹ The remaining crude soy oil undergoes further refining—including degumming, neutralization, bleaching, and deodorization—to produce the clear, odorless, and flavorless product sold as “vegetable oil”.¹ Meanwhile, the defatted flakes enter a machine called a desolventizer-toaster. Here, multiple decks of steam-heated trays heat the flakes, boiling off the residual hexane for recovery. The process also toasts the meal, which improves its nutritional value and digestibility for animals.¹

From a single 60-pound bushel of soybeans, this process yields approximately 47 pounds of soybean meal and 12 pounds of oil.¹⁹ While processing efficiencies and bean composition can cause slight variations, the fundamental output remains consistent.²⁰ While the oil is a valuable commodity, it is the meal that has become the primary economic driver of the entire industry. An estimated 70% of the soybean’s total value is derived from its meal, which represents two-thirds of the global output of protein feedstuffs.¹,²¹

The Hidden Ingredient: Fueling the Meat Machine

The single most important fact for understanding the modern soy industry is its ultimate customer. While soy is often associated with tofu, soy milk, and other plant-based foods, these products represent a tiny fraction of its use. Only about 6-7% of soybeans grown worldwide are turned directly into food for human consumption.²²,²³ The overwhelming majority—an astonishing 70% to 77% of the entire global crop—is destined for the feed trough.²⁴,²⁵ In the United States, the proportion is even more stark, with over 90% of the domestic crop used for animal feed.¹

This high-protein soybean meal is a foundational ingredient in modern, intensive animal agriculture. It is the primary protein source for the world’s chickens, pigs, dairy and beef cattle, and farmed fish, valued for its superior amino acid profile and digestibility.¹,²¹ The global demand for soy, therefore, is not driven by a surge in vegetarianism, but by the world’s growing appetite for meat, eggs, and dairy. This relationship is so direct that soy demand serves as a proxy for meat consumption. The explosive growth of the livestock sector in nations like China, now the world’s largest importer of soybeans, has single-handedly reshaped global agricultural landscapes.²⁶,²⁷

The industrial logic is inescapable. The soy crushing industry and the industrial livestock industry did not merely grow in parallel; they co-evolved into a deeply symbiotic system. The efficiency of the crushing process, which perfectly bifurcates the bean into a neutral oil for the processed food sector and a protein-rich meal for the livestock sector, allowed both industries to scale at an unprecedented rate. The soaring global demand for cheap meat transformed soybean meal from a simple byproduct into the industry’s most valuable commodity. As the United Nations Food and Agriculture Organization (FAO) predicts that global consumption of poultry, pork, and aquaculture will continue to climb, the demand for soy is projected to increase dramatically in lockstep. One FAO projection estimates a rise from 276 million metric tons in 2013 to 390 million by 2050, while another suggests a 140% increase to 515 million tonnes over a similar period.²⁴,²⁸ Consequently, any serious conversation about the sustainability of soy is, by necessity, a conversation about the sustainability of the global industrial meat production system it so efficiently fuels.

Part II: The Planetary Toll: Ecosystem Degradation and Public Health Crises

The relentless expansion of the soy industry, driven by the global demand for animal feed, has cast a long and destructive shadow across the planet. This expansion is a story of vanishing forests, of a deluge of agricultural chemicals contaminating ecosystems and communities, and of a profound social cost borne by those living on the agricultural frontier. The industry’s environmental strategy has exhibited a pattern of “problem-shifting” rather than problem-solving. This creates “sacrificial zones”—both ecologically, in the case of the Cerrado, and in terms of human health for downstream communities—where the true costs of production are borne by the vulnerable and politically voiceless. This reframes the issue from one of simple environmental damage to one of profound environmental injustice.

The Vanishing Forests: A Tale of Two Biomes

The narrative of soy and deforestation is most famously set in the Brazilian Amazon. In the early 2000s, the crop became a primary driver of rainforest destruction, as forests were cleared to make way for vast monoculture plantations.¹ The ensuing global outcry, spearheaded by a 2006 Greenpeace report titled “Eating up the Amazon,” directly linked major food companies like McDonald’s to this destruction.¹ This pressure campaign culminated in a landmark achievement: the Amazon Soy Moratorium (ASM). First signed in 2006 and renewed indefinitely, this voluntary agreement between major grain traders, civil society, and the Brazilian government committed signatories to not purchase soy grown on Amazon land deforested after 2008.¹

By its own narrow metric, the ASM has been a stunning success. Direct conversion of Amazon rainforest for soy cultivation plummeted, accounting for less than 1% of soy expansion in the biome by 2014.¹ However, this celebrated victory masks a more complex and troubling reality. The moratorium contains a critical loophole: it allows soy to be planted on land that was previously cleared, most often for cattle pasture. This has created a powerful economic incentive for soy farmers to buy up existing pastureland, which in turn pushes cattle ranchers deeper into the forest frontier, where they clear new areas of rainforest for their herds. In this way, soy cultivation remains a powerful indirect driver of Amazon deforestation, a phenomenon some have called “cattle laundering”.²⁹,³⁰,³¹

The most significant failing of the ASM, however, is not a loophole but a boundary. The agreement applies only to the Amazon biome. It offers no protection for the Cerrado, a sprawling tropical savanna to the south and east of the Amazon that is one of the most biodiverse ecosystems of its kind on Earth.¹,⁷ While the world’s attention was fixed on the rainforest, the soy frontier simply shifted. Capital, technology, and agricultural machinery flowed into the path of least resistance: the vast, unprotected plains of the Cerrado.³² This has allowed soy traders to market their product as “Amazon-deforestation-free” while simultaneously presiding over the systematic destruction of another globally critical ecosystem.¹ The ASM did not end soy-driven land conversion; it merely relocated it, creating a perverse incentive to sacrifice one biome to save another.

A Chemical Deluge: The Environmental and Human Cost of Pesticides

The ecological footprint of soy extends far beyond land use change. The industry’s near-total reliance on GM herbicide-tolerant varieties has locked farmers into a system of intensive chemical agriculture.¹ In the United States, 98% of soybean acreage is treated with herbicides, with glyphosate being the most common.¹ This monoculture system, a veritable buffet for pests, also necessitates the heavy use of insecticides and fungicides.¹

These agrochemicals inevitably migrate from the fields into the wider environment. Agricultural runoff carries pesticides and excess fertilizer into rivers, streams, and lakes, where they contaminate water supplies, harm aquatic life, and contribute to the formation of oxygen-depleted “dead zones”.³³,³⁴ Studies in Argentina have documented high concentrations of insecticides like endosulfan and chlorpyrifos in streams adjacent to soy fields, correlating directly with a sharp decline in fish diversity and 100% mortality rates for key aquatic invertebrates.¹ The chemicals also bind to soil particles, where they can persist for long periods, degrading soil health and contaminating groundwater.³⁵

The most devastating consequence of this chemical deluge is its impact on human health. For years, communities in the soy-producing regions of South America have reported clusters of cancers, birth defects, and other serious illnesses.¹,³⁶ These anecdotal fears have now been substantiated by rigorous scientific research, though the findings require precise characterization. A landmark 2023 study published in the Proceedings of the National Academy of Sciences (PNAS) by Skidmore et al. established a statistically significant association between the expansion of soy cultivation in Brazil and a rise in childhood deaths from acute lymphoblastic leukemia (ALL), the most common form of childhood cancer.³⁷,³⁸

The study’s findings are harrowing. It estimated that approximately half of all pediatric leukemia deaths in the Amazon and Cerrado soy frontiers between 2008 and 2019—a total of 123 deaths of children under the age of 10—were associated with exposure to the pesticides used in soy farming.³⁹,⁴⁰ The researchers identified the primary pathway of exposure as contaminated water. By analyzing river networks, they demonstrated that soy production upstream in a watershed was directly correlated with leukemia deaths in communities downstream, indicating that pesticide runoff is poisoning the water supply for entire regions.³⁷,⁴⁰

For scientific accuracy and legal defensibility, it is crucial to note the study’s methodological limitations. As lead author Marin Skidmore explicitly stated, “the study doesn’t provide a direct, causal link between pesticide exposure and cancer deaths”.¹ The observational, ecological design of the research can identify powerful correlations but cannot definitively prove causation. However, this distinction does not diminish the gravity of the findings. The study provides the kind of strong associative evidence that often forms the basis for precautionary public health policy. Prominent epidemiologists have called the findings “alarming data” warranting urgent further investigation.¹ The high bar for proving direct causality in human populations often results in regulatory paralysis, forcing vulnerable communities to bear the burden of risk while science plays catch-up. The PNAS study represents a critical signal that the chemical-intensive model of soy production poses a grave and potentially lethal threat to public health.

This public health crisis is further compounded by social and geographic inequality. The study found that the lethal effect of this exposure was concentrated in municipalities located more than 100 kilometers (about 62 miles) from a specialized cancer treatment center, where a lack of access to care turns a treatable disease into a death sentence.³⁷,³⁹ In addition to this silent poisoning, communities on the agricultural frontier, particularly Indigenous and traditional groups, often face direct violence, intimidation, and forced displacement as agribusiness operations expand onto their lands.¹

Part III: The Architecture of Power: Geopolitics and Corporate Consolidation

The soy industry is not a diffuse network of independent farmers and traders; it is a global leviathan, a highly concentrated system of geopolitical and corporate power. A small number of nations dominate its production, a few key markets drive its demand, and a secretive oligopoly of multinational corporations controls its trade, reaping immense profits from this ubiquitous bean.

The Soy Superpowers: A Global Map of Production and Consumption

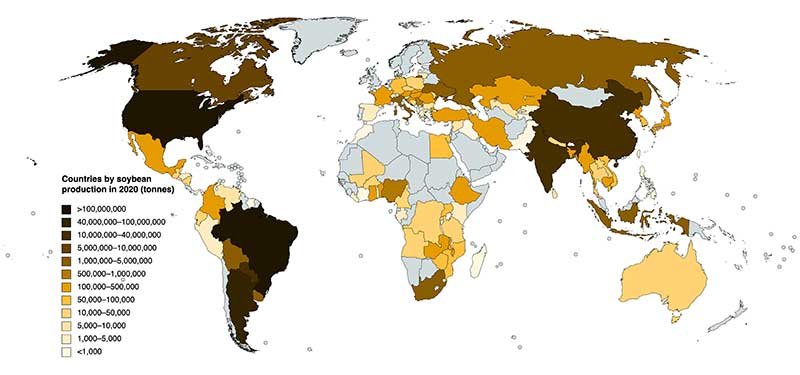

The world of soy production is a club with very few members. Three nations—Brazil, the United States, and Argentina—collectively account for roughly 80% of the entire global harvest.⁴¹ In 2022, Brazil officially surpassed the U.S. to become the world’s largest producer, responsible for 35% of the total, with the U.S. close behind at 33%.¹ Projections for the 2024/2025 marketing year show Brazil solidifying this lead, expected to produce 169 million metric tons, or 40% of the global total.⁴²

This massive productive capacity exists to serve an equally concentrated demand. The entire global soy complex is oriented towards a few key import markets. The People’s Republic of China is the undisputed center of gravity, importing a colossal 95.5 million metric tons in 2021 alone—more than the next several largest importers combined.⁴³,⁴⁴ This demand is almost entirely driven by China’s massive and expanding livestock industry, which requires vast quantities of soybean meal for animal feed.¹,²⁷ The European Union is the second-largest import market. Though often invisible to the end consumer, soy is deeply embedded in the European diet; the average European consumes over 60 kg of soy per year, with 90% of it “hidden” within the meat, dairy, fish, and eggs it was used to produce.¹

For a nation like Brazil, soy is an economic juggernaut. It was the country’s second-largest export in 2023, generating nearly US$53 billion in revenue and representing 16% of all exports.¹ The crop’s expansion has been a primary driver of Brazil’s transformation from a food importer into a global agricultural superpower.¹ This economic boom, however, has come at a steep price, fueling deforestation, compromising water security, and displacing the production of staple food crops for domestic consumption in favor of an export-oriented monoculture.¹

Table 1: Global Soybean Production by Top Nations (2024/2025 Projections)

| Country | Production (Million Metric Tons) | % of Global Production |

| Brazil | 169.00 | 40% |

| United States | 118.84 | 28% |

| Argentina | 50.90 | 12% |

| China | 20.65 | 5% |

| India | 12.58 | 3% |

| Source: USDA Foreign Agricultural Service.⁴² |

The Merchants of Soy: The ‘ABCD’ Oligopoly

Connecting the soy fields of the Americas to the feed mills of Asia and Europe is a small group of immensely powerful, and often intensely private, multinational corporations. The global grain trade is an oligopoly, dominated by four companies known collectively as the “ABCDs”: Archer-Daniels-Midland (ADM), Bunge, Cargill, and Louis Dreyfus Company.¹ Together, these four giants control an estimated 70-90% of the international trade in key agricultural commodities, including soybeans.⁴⁵,⁴⁶

Their power stems from their vertical integration across the entire supply chain. These are not merely trading houses; they are deeply involved in every step of the process, from financing farmers and selling them seeds and fertilizers to owning the vast infrastructure of grain elevators, processing plants, port terminals, and ocean-going vessels.¹,⁴⁶ This control over the logistical “choke points” of global trade gives them enormous leverage to influence prices and dictate terms. They are the indispensable, and often invisible, intermediaries of the global food system. They are joined in this top tier by other massive players, most notably the Chinese state-owned enterprise COFCO International and the Singapore-based Wilmar International.¹

Table 2: The Soy Trade Oligopoly

| Company | Headquarters | Estimated Combined Share of Global Grain Trade |

| Archer-Daniels-Midland (ADM) | Chicago, USA | 70-90% (collectively) |

| Bunge | St. Louis, USA | |

| Cargill | Minnetonka, USA | |

| Louis Dreyfus Company | Rotterdam, Netherlands | |

| Source: The Guardian; World Bio Market Insights.⁴⁵,⁴⁶ |

Valuation of a Titan: The Economics of the Bean

The economic scale of the soy industry is staggering. In 2023, the global soybean market was valued at approximately USD 193.1 billion, with forecasts projecting growth to over USD 258 billion by 2030 and potentially as high as USD 388 billion by 2034.⁴⁷,⁴⁸ This reflects a robust compound annual growth rate (CAGR) of between 4.4% and 6.2%.⁴⁷,⁴⁸

An analysis of the market’s structure confirms the industry’s defining characteristics. The market is overwhelmingly dominated by:

- Processed Soybeans: These products (meal, oil, etc.) account for 84.5% of market revenue, underscoring the industrial nature of the crop.⁴⁷

- Genetically Modified (GM) Soybeans: GM varieties make up 84% of the market, highlighting the industry’s deep reliance on biotechnology.⁴⁸

- Animal Feed: The animal feed segment is the largest end-use category, commanding 73% of the market share.⁴⁸

Geographically, the Asia-Pacific region represents the largest market, accounting for over 40% of the total, a direct reflection of China’s immense import demand for livestock feed.⁴⁷,⁴⁹ The entire economic edifice of the modern soy industry is thus built on a foundation of genetically modified beans, industrially processed into animal feed, and shipped across the globe to fuel the production of meat and dairy.

Part IV: The Crisis of Accountability: A Decade of Ineffectual Self-Regulation

As awareness of the soy industry’s destructive footprint has grown, so too have calls for reform. Yet the path toward sustainability has been fraught with broken promises, ineffective certification schemes, and documented inconsistencies between corporate pledges and on-the-ground reality. The architecture of corporate self-regulation in the soy industry has not merely failed; it has functioned as a sophisticated system for managing perception and deflecting accountability. Mechanisms like certification credits create a parallel, virtual market for “sustainability” that allows the physical market of destructive extraction to continue undisrupted, exposing the profound limitations of voluntary self-regulation and pointing toward the necessity of more fundamental, systemic change.

The Promise and Peril of Pledges: A Decade of Failure

The early 2010s saw a wave of optimism as hundreds of major corporations, organized under platforms like the Consumer Goods Forum, pledged to achieve “zero net deforestation” in their supply chains by 2020.¹ These commitments covered key forest-risk commodities, including soy. A decade later, the results were in, and the verdict was damning. A 2019 Greenpeace International investigation concluded that the corporate pledge movement had been a “total disaster”.⁵⁰ By the start of 2020, an area of forest the size of Spain—at least 50 million hectares—was estimated to have been destroyed for commodity production since the promises were first made.⁵¹

The failure was systemic. Greenpeace found that not a single company it contacted could demonstrate a “meaningful effort” to eradicate deforestation from its supply chain. The most fundamental obstacles were a pervasive lack of traceability—companies often did not know the specific farms their soy came from—and a colossal blind spot regarding the vast quantities of soy embedded in their animal feed supply chains.⁵⁰ This assessment was echoed by a 2021 Soy Traders Scorecard from the World Wide Fund for Nature (WWF). The first-of-its-kind study evaluated 22 of the world’s most influential soy traders and found that none were taking sufficient action on their environmental and social commitments. The highest-scoring company achieved a grade of just 52.5%, a clear failure across the board.¹ The decade of voluntary pledges had produced more press releases than progress, exposing the inadequacy of corporate self-regulation in the face of powerful economic incentives to maintain the status quo.

Certifying a Smokescreen? The Case of the RTRS

The primary industry-led mechanism for sustainability is the Round Table on Responsible Soy (RTRS), a multi-stakeholder initiative founded in 2006 to create a certification standard for “responsible” soy production.¹ The RTRS standard covers principles such as environmental responsibility and fair labor conditions, and in 2016, it incorporated a “zero deforestation/zero conversion” criterion.¹

Despite its stated mission, independent investigations and academic research have documented significant structural limitations in the RTRS certification system. Critics from a broad coalition of environmental and social organizations have characterized it as a “smokescreen” that provides a veneer of sustainability while legitimizing destructive business-as-usual practices.⁵²,⁵³ The core criticisms are numerous and fundamental.

First is the system of “credits.” According to multiple sources, including investigative reports from Earthsight and Planet Tracker, the vast majority—over 90%—of RTRS-certified material is traded not as physically segregated soy but as credits.⁵⁴,⁵⁵ A company can continue to buy soy from any source, regardless of its link to deforestation, and then purchase RTRS credits on a separate market to “offset” its footprint and claim it is “supporting responsible soy production.” This system decouples the sustainability claim from the physical supply chain, allowing companies to appear green without actually cleaning up their sourcing. It creates a parallel, virtual market for “sustainability” that allows the physical market of destructive extraction to continue undisrupted.¹,⁵⁴

Second, the standards themselves have been condemned as weak. The RTRS criteria have been criticized for allowing deforestation in vital ecosystems like the Cerrado as long as the land is legally “zoned” for agriculture, effectively rubber-stamping the conversion of critical habitats. Furthermore, the standard is “technology neutral,” which means it certifies the very GM herbicide-tolerant soy monocultures that drive the industry’s chemical dependency.⁵²

Finally, even with these standards, enforcement appears to be lacking. An October 2024 investigation by Earthsight, titled “Secret Ingredient,” documented RTRS-certified farms implicated in apparent illegal deforestation, corruption, and land grabbing. For example, it found that farms belonging to the Franciosi Agro group were certified despite the company clearing 5,000 hectares of forest elsewhere, 3,000 of which were apparently illegal. Another certified producer, the Horita Group, was linked to a major land-grabbing scandal.⁵⁴ In response to these public revelations, RTRS suspended the certifications pending investigation, demonstrating a reactive rather than proactive enforcement posture.⁵⁴ The situation has become so untenable that even WWF Netherlands, an original founding partner of the RTRS, publicly declared in 2021 that it had “lost confidence” in the scheme’s ability to combat deforestation, a major blow to the standard’s credibility.¹

Corporate Pledges vs. On-the-Ground Reality: A Case Study of Cargill

The actions of Cargill, one of the world’s largest and most powerful soy traders, provide a stark case study in the inconsistencies between corporate sustainability rhetoric and documented supply chain practices. Despite public commitments to achieve deforestation-free supply chains, the company has been persistently linked to deforestation in the Brazilian Cerrado and implicated in the social and environmental harms associated with its operations.¹

In May 2023, the environmental law non-profit ClientEarth filed a formal complaint with the U.S. National Contact Point (NCP) under the OECD Guidelines for Multinational Enterprises, alleging inadequate environmental due diligence in Cargill’s soy operations.⁵⁶ While the complaint was ultimately rejected on procedural grounds in January 2025—specifically, a lack of authorized representation for the affected Brazilian communities—the NCP simultaneously issued a public statement recommending that Cargill strengthen its due diligence practices, a nuanced outcome that acknowledged shortcomings in the company’s processes.⁵⁷

Multiple NGO investigations have documented what they characterize as systematic gaps in Cargill’s supply chain monitoring. ClientEarth’s complaint asserted that Cargill does not adequately monitor the 42% of its Brazilian soy that it buys from third-party traders.⁵⁸ This finding is echoed in reports from Global Witness and Greenpeace, which have documented continued sourcing from farms engaged in deforestation.¹ The core inconsistency in Cargill’s approach is geographic. While the company adheres to the Amazon Soy Moratorium, it has repeatedly rejected proposals for an equivalent moratorium to protect the far more threatened Cerrado biome, where it has been identified as the largest exporter.⁵⁸ This selective application of sustainability policies allows the company to maintain a public posture of responsibility in one region while profiting from ecosystem destruction in another. This strategy appears focused more on reputational risk management than on genuine systemic reform, applying real measures only where public scrutiny is highest while using rhetoric and weaker systems elsewhere.

Cargill has responded to these criticisms by highlighting its sustainability commitments, stating that 93.72% of its sourced volume is deforestation-free, and acknowledging that “we have further to go”.⁵⁷ However, the pattern of documented behavior suggests a corporate strategy that addresses public pressure points without disrupting the core, profitable business model of sourcing cheap commodities at scale.

Farming for the Future: Pathways to Regeneration

Amidst the failures of corporate pledges and certification schemes, a more hopeful path is emerging from the ground up. A growing movement is advocating for a shift away from merely “sustainable” agriculture—which can imply sustaining a degraded system—toward “regenerative” agriculture, which aims to actively restore soil health, biodiversity, and ecosystem function. Several key practices are directly applicable to soybean farming:

- No-Till and Strip-Till Farming: This practice involves planting seeds directly into the residue of the previous year’s crop without plowing the soil. By leaving the soil structure intact, no-till farming dramatically reduces erosion by wind and water, increases the soil’s capacity to absorb and retain moisture, builds up organic matter, and sequesters atmospheric carbon in the soil.⁵⁹,⁶⁰

- Cover Cropping: Instead of leaving fields bare in the off-season, farmers plant “cover crops” like cereal rye or oats. These crops keep living roots in the soil year-round, protecting it from erosion, suppressing weeds, and capturing nutrients that might otherwise leach into waterways. When the cover crop is terminated before planting the main cash crop, it decomposes, adding valuable organic matter back into the soil.⁵⁹,⁶⁰

- Complex Crop Rotation: Moving beyond the standard two-year corn-soy rotation to include other crops like wheat, alfalfa, or clover helps to break pest and disease cycles naturally, reducing the need for chemical interventions. It also diversifies the “diet” for the soil microbiome, enhancing soil health.⁵⁹,⁶¹

- Precision Agriculture: This involves using modern technology—such as GPS-guided tractors, satellite imagery, and soil sensors—to apply fertilizer and pesticides with pinpoint accuracy, only where and when they are needed. This approach can significantly reduce the total volume of chemical inputs, saving farmers money and minimizing environmental runoff.⁵⁹

These practices offer a pathway to a fundamentally different kind of agriculture. They not only mitigate the environmental damage of conventional farming but can also enhance farm profitability and, crucially, build resilience to the extreme weather events, such as droughts and floods, that are becoming more frequent in a changing climate.⁵⁹

Conclusion: Mandating a Regenerative Future

The journey of the soybean is a parable for our times. It is a story of an agricultural marvel, a plant of immense potential, that was harnessed by an industrial logic that optimized for efficiency and profit while systematically ignoring the costs to the planet and its people. The result is the two-faced bean: a cornerstone of global food security that has become a potent vector for ecological and social fracturing.

This investigation has shown that the modern soy industry is fundamentally an appendage of the global industrial meat machine; that its environmental footprint, having scarred the Amazon, is now consuming the Cerrado savanna; that its dependence on agrochemicals is fueling a public health crisis in rural communities, evidenced by a strong statistical association with childhood cancer mortality; and that its attempts at self-regulation have been largely performative, a “smokescreen” of pledges and certifications that obscures a destructive reality. The history of the soy industry makes one thing clear: voluntary self-regulation has proven to be a failed experiment. Meaningful change will not be offered voluntarily; it must be demanded and, ultimately, mandated.

Improving the soy industry’s role as a corporate citizen requires a comprehensive, multi-pronged strategy that moves decisively beyond this failed model. The path forward must be built on a foundation of accountability, transparency, and a fundamental redesign of the agricultural systems themselves.

First, binding regulation is essential. The era of voluntary pledges must end. Enforceable, government-led legislation, such as the European Union’s 2023 regulation banning the import of commodities linked to deforestation, is a critical first step. Such laws create a level playing field, making sustainability a non-negotiable condition of market access rather than a voluntary add-on.³¹

Second, radical supply chain transparency must be mandated. The technology exists to trace commodities from the specific farm plot where they were grown all the way to the end consumer. This traceability must be demanded by major buyers, investors, and governments to eliminate the loopholes and “laundering” practices that allow deforestation to remain hidden within complex supply chains.

Third, the financial sector must be held accountable. The global banks and investment firms that provide the capital for agricultural expansion are complicit in its consequences. These institutions must be pressured—by regulators and their own shareholders—to use their immense leverage to require that clients adopt, implement, and independently verify credible, time-bound “zero conversion” policies that protect all native ecosystems, not just forests.

Fourth, a systemic shift toward regenerative agriculture must be accelerated. This requires more than just individual farmer adoption; it demands public and private investment in research, technical assistance, and financial incentives—such as crop insurance discounts or carbon credits—that make it economically rational for farmers to transition to practices that rebuild soil health, protect water, and enhance biodiversity.⁶¹

Finally, and most challengingly, the world must confront the ultimate driver of the problem: unsustainable levels of global meat consumption. As long as the demand for cheap, industrially produced animal protein continues its relentless climb, the pressure on landscapes to produce feed will be immense. Encouraging dietary shifts toward more plant-rich foods is not a peripheral issue; it is central to alleviating the pressure that the soy leviathan exerts on the planet.

The humble soybean is not inherently destructive. Its future, and in many ways the future of the landscapes it occupies, depends on our collective ability to reimagine its purpose. The challenge is to transform it from a symbol of hidden costs and externalized harm into a source of genuine, equitable, and regenerative nourishment for a growing world.

Notes

- User-Provided Document, “The Two-Faced Bean: An Investigation into the Global Soy Industry’s Impact on Ecosystems, Health, and Corporate Governance,” October 2024.

- United Soybean Board, “Industrial Uses,” Issue Briefs, accessed October 2024, https://unitedsoybean.org/issue-briefs/industrial-uses/.

- Allergic Living, “The Scoop on Why Soy’s in So Many Products,” September 2, 2010, https://www.allergicliving.com/2010/09/02/the-scoop-on-why-soys-in-so-many-products/.

- New York Agriculture in the Classroom, “Soybeans,” Empire Agriculture Map, accessed October 2024, https://newyork.agclassroom.org/empire-agriculture-map/agricultural-products/soybeans/.

- S. Walley et al., “Nitrogen Fixation by Legumes,” New Mexico State University, Publication A-129, accessed October 2024, https://pubs.nmsu.edu/_a/A129/.

- Luiz Felipe A. Almeida et al., “Soybean Inoculation and Nitrogen Fixation,” Soybean Science for Success, May 14, 2025, https://soybeanscienceforsuccess.org/2025/05/14/soybean-inoculation-and-nitrogen-fixation/.

- World Wide Fund for Nature, “Soy,” WWF Global, accessed October 2024, https://wwf.panda.org/discover/our_focus/food_practice/sustainable_production/soy/.

- International Service for the Acquisition of Agri-biotech Applications, “Global Status of Commercialized Biotech/GM Crops: 2019,” ISAAA Brief No. 55, 2019, https://www.isaaa.org/resources/publications/briefs/55/executivesummary/default.asp.

- U.S. Department of Agriculture, Economic Research Service, “Recent Trends in GE Adoption,” Adoption of Genetically Engineered Crops in the United States, last modified January 4, 2025, https://www.ers.usda.gov/data-products/adoption-of-genetically-engineered-crops-in-the-united-states/recent-trends-in-ge-adoption.

- Bayer Crop Science, “Soybean Growth Stages,” Bayer US, accessed October 2024, https://www.cropscience.bayer.us/articles/bayer/soybean-growth-stages.

- Seth L. Naeve, “Soybean growth stages,” University of Minnesota Extension, last reviewed 2018, https://extension.umn.edu/growing-soybean/soybean-growth-stages.

- Chad Lee and James Herbek, “Soybean Growth and Development,” University of Kentucky College of Agriculture, Food and Environment, AGR-223, accessed October 2024,(http://www2.ca.uky.edu/agc/pubs/AGR/AGR223/AGR223.pdf).

- W. R. Fehr and C. E. Caviness, “Stages of Soybean Development,” Iowa State University, Special Report 80, 1977.

- University of Minnesota Extension, “Soybean growth stages,” accessed October 2024, https://extension.umn.edu/growing-soybean/soybean-growth-stages.

- V. Gibon et al., “Current technologies for the extraction and refining of edible oils,” OCL – Oilseeds and fats, Crops and Lipids 27, no. 49 (2020), https://www.ocl-journal.org/articles/ocl/full_html/2020/01/ocl200047s/ocl200047s.html.

- AOCS, “Solvent Extraction,” American Oil Chemists’ Society, accessed October 2024, https://www.aocs.org/resource/solvent-extraction/.

- AOCS, “Solvent Extraction.”

- Audrey Cosson et al., “Hexane: A Neurotoxic Solvent Used in the Food Industry without Consumer’s Knowledge,” Foods 11, no. 22 (2022): 3698, https://pmc.ncbi.nlm.nih.gov/articles/PMC9655691/.

- American Soybean Association, “Soy Stats 2024,” June 2024,(https://soygrowers.com/wp-content/uploads/2024/06/24ASA-001-Soy-Stats-Web.pdf).

- Scott Irwin, “The Soybean Industry Response to the Renewable Diesel Boom, Part 1: The Long-Run Evolution of Oilseed Crushing,” Agriculture.com, accessed October 2024, https://www.agriculture.com/partners-the-soybean-industry-response-to-the-renewable-diesel-boom-part-1-the-long-run-evolution-of-oilseed-crushing-11797457.

- U.S. Soybean Export Council, “Soybean Meal,” USSEC, accessed October 2024, https://ussec.org/why-choose-us-soy/soybean-meal/.

- Union of Concerned Scientists, “Soybeans,” accessed October 2024, https://www.ucs.org/resources/soybeans.

- Hannah Ritchie, “More than three-quarters of global soy is fed to animals,” Our World in Data, last updated August 2021, https://ourworldindata.org/soy.

- Union of Concerned Scientists, “Soybeans.”

- Food and Agriculture Reform for the Millennium, “Soy: food, feed, and land use change,” TABLE Debates, December 2021,(https://www.tabledebates.org/sites/default/files/2021-12/FCRN%20Building%20Block%20-%20Soy_food,%20feed,%20and%20land%20use%20change%20(1).pdf).

- Dora Marinova and Diana Bogueva, “Soy Production and Consumption in China,” in Sustainable Consumption and Production in the Asia-Pacific (Singapore: Springer, 2019), https://espace.curtin.edu.au/bitstream/handle/20.500.11937/88226/88048.pdf.

- Sara Warden, “Biofuels to Overtake China as Soybean Demand Driver,” Czapp, accessed October 2024, https://www.czapp.com/analyst-insights/biofuels-to-overtake-china-as-soybean-demand-driver/.

- Jelle Bruinsma, ed., “World agriculture: towards 2030/2050 – The 2012 Revision,” Food and Agriculture Organization of the United Nations, ESA Working Paper No. 12-03, June 2012, https://www.fao.org/4/i2280e/i2280e06.pdf.

- Karla Mendes, “Enforce Brazilian laws to curb criminal Amazon deforestation: study,” Mongabay, November 4, 2019, https://news.mongabay.com/2019/11/enforce-brazilian-laws-to-curb-criminal-amazon-deforestation-study/.

- CEBRI and Insper Agro Global, “Decoupling Soy and Beef Production from Illegal Amazon Deforestation,” March 2021,(https://www.cebri.org/media/documentos/arquivos/Relatorio_CEBRI-Insper_22mar605a09c1c3da0.pdf).

- Forests of the World, “Soy,” Forest Clearing, accessed October 2024, https://www.forestsoftheworld.org/forest-clearing/soy/.

- Hannah Ritchie, “Drivers of Deforestation,” Our World in Data, last updated February 2024, https://ourworldindata.org/drivers-of-deforestation.

- M. A. S. van der Meulen and G. G. M. Schulten, “Glyphosate in the environment: A review of its fate, effects, and potential risks,” Frontiers in Environmental Science 9 (2021): 763917, https://www.frontiersin.org/journals/environmental-science/articles/10.3389/fenvs.2021.763917/full.

- M. C. Z. de Souza et al., “Glyphosate and Its Formulations: A Global Threat to Human and Environmental Health,” Sustainability 14, no. 11 (2022): 6868, https://www.mdpi.com/2071-1050/14/11/6868.

- John P. Myers et al., “Concerns over use of glyphosate-based herbicides and risks associated with exposures: a consensus statement,” Environmental Health 15, no. 19 (2016), https://pmc.ncbi.nlm.nih.gov/articles/PMC4756530/.

- Anna Ortega, “The sick children of Brazilian agriculture,” Diálogo Chino, accessed October 2024, https://dialogue.earth/en/food/the-sick-children-of-brazilian-agriculture/.

- Marin Elisabeth Skidmore et al., “Agricultural intensification and childhood cancer in Brazil,” Proceedings of the National Academy of Sciences 120, no. 45 (2023): e2306003120, https://pmc.ncbi.nlm.nih.gov/articles/PMC10636353/.

- Skidmore et al., “Agricultural intensification.”

- Spoorthy Raman, “Study links pesticides to child cancer deaths in Brazilian Amazon, Cerrado,” Mongabay, November 27, 2023, https://news.mongabay.com/2023/11/study-links-pesticides-to-child-cancer-deaths-in-brazilian-amazon-cerrado/.

- Marianne Stein, “Soy expansion in Brazil linked to increase in childhood leukemia deaths,” University of Illinois College of ACES News, October 30, 2023, https://aces.illinois.edu/news/soy-expansion-brazil-linked-increase-childhood-leukemia-deaths.

- Thomas R. DeGregori, “Growth of the soybean frontier in South America: The case of Brazil and Argentina,” Revista de Historia Económica – Journal of Iberian and Latin American Economic History 38, no. 3 (2020): 487–514,(https://www.cambridge.org/core/journals/revista-de-historia-economica-journal-of-iberian-and-latin-american-economic-history/article/growth-of-the-soybean-frontier-in-south-america-the-case-of-brazil-and-argentina/CE2821B827BB619EDB57E47416940408).

- U.S. Department of Agriculture, Foreign Agricultural Service, “Soybeans: World Markets and Trade,” October 2024, https://www.fas.usda.gov/data/production/commodity/2222000.

- International Institute for Sustainable Development, “Global Market Report: Soybean,” February 2024, https://www.iisd.org/system/files/2024-02/2024-global-market-report-soybean.pdf.

- Trading Economics, “Soybeans,” accessed October 2024, https://tradingeconomics.com/commodity/soybeans.

- Joseph Winters, “Record profits for grain firms amid food crisis prompt calls for windfall tax,” The Guardian, August 23, 2022, https://www.theguardian.com/environment/2022/aug/23/record-profits-grain-firms-food-crisis-calls-windfall-tax.

- World Bio Market Insights, “The ABCD Agro-Giants: Hidden Movers in Biobased Scaling,” accessed October 2024, https://worldbiomarketinsights.com/the-abcd-agro-giants-hidden-movers-in-biobased-scaling/.

- Grand View Research, “Soybean Market Size, Share & Growth Analysis Report, 2030,” Report ID: GVR-1-68038-892-0, January 2024, https://www.grandviewresearch.com/industry-analysis/soybean-market-report.

- Precedence Research, “Soybean Market Size to Hit USD 388.33 Billion by 2034,” Report ID: 3548, October 2024, https://www.precedenceresearch.com/soybean-market.

- IndustryARC, “Soybean Market – Forecast(2025 – 2031),” Report Code: FBR 0081, July 2024,(https://www.industryarc.com/Report/18471/soybean-market-research-report-analysis.html).

- Rhett A. Butler, “Despite a decade of zero-deforestation vows, forest loss continues: Greenpeace,” Mongabay, June 11, 2019, https://news.mongabay.com/2019/06/despite-a-decade-of-zero-deforestation-vows-forest-loss-continues-greenpeace/.

- Greenpeace International, “50 million hectares destroyed as companies disregard zero deforestation pledge,” Press Release, June 11, 2019, https://www.greenpeace.org/international/press-release/22287/50-million-hectares-destroyed-as-companies-disregard-zero-deforestation-pledge/.

- Corporate Europe Observatory, “Roundtable on Responsible Soy – the certification smokescreen,” May 22, 2012, https://corporateeurope.org/en/agribusiness/2012/05/roundtable-responsible-soy-certification-smokescreen.

- Thünen Institute, “Sustainability certification of soy: The Round Table on Responsible Soy,” accessed October 2024, https://www.thuenen.de/en/themenfelder/maerkte-handel-zertifizierung/nachhaltigkeitsstandards-und-zertifizierungssysteme/sustainability-certification-of-soy-the-round-table-on-responsible-soy.

- Earthsight, “How sustainable is sustainable soy?” Earthsight News, October 2024, https://www.earthsight.org.uk/news/sustainable-soy.

- Planet Tracker, “Increased soy certification would decrease deforestation risk,” March 2022, https://planet-tracker.org/increased-soy-certification-would-decrease-deforestation-risk/.

- ClientEarth, “ClientEarth vs. Cargill,” Climate Case Chart, last updated May 5, 2024, https://climatecasechart.com/non-us-case/clientearth-vs-cargill/.

- U.S. Department of State, “Final Statement: Specific Instance between ClientEarth (Submitter) and Cargill, Incorporated regarding operations in Brazil,” January 17, 2025, https://www.state.gov/specific-instance-between-clientearth-submitter-and-cargill-incorporated-regarding-operations-in-brazil.

- U.S. Department of State, “Final Statement.”

- Syngenta Group, “Regenerative Agriculture,” accessed October 2024, https://www.syngentagroup.com/regenerative-agriculture.

- Kurtis Dop, “Embedding regenerative agriculture practices to seed production sites,” Syngenta News Service, May 2025, https://www.syngenta.com/agriculture/sustainable-agriculture/embedding-regenerative-agriculture-practices-to-seed-production-sites.

- Mark Liebig and Matthew C. Ryan, “The Economics of Regenerative Agriculture,” USDA Agricultural Research Service, accessed October 2024, https://www.ars.usda.gov/oc/utm/the-economics-of-regenerative-agriculture.

{kind=link}